Click Here to view Pension Report Overview

Last year, Illinois taxpayers were funding million-dollar pension payouts for 148,654 retired government employees. That number for our 15th annual pension study has since climbed to 151,391.

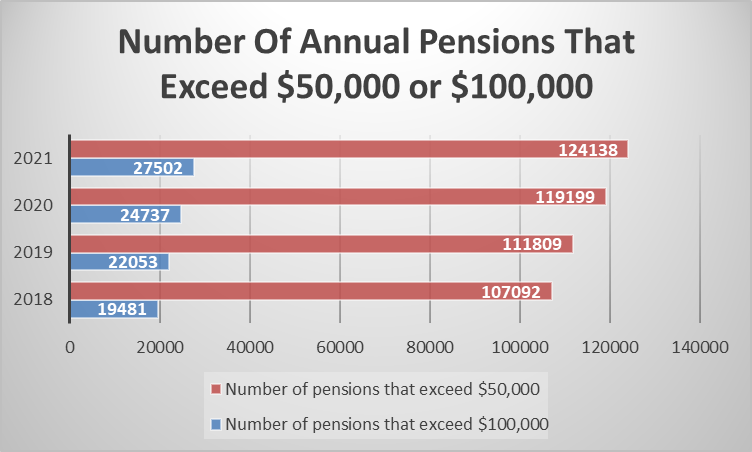

These pensions are not small. According to information provided by the pension funds, 124,138 of these pensions meet or exceed an annual payout of $50,000. 27,502 of these pensions also exceed $100,000 annually. This is because the vast majority of Illinois government pensions are subject to a 3% compounded cost of living adjustment. This compounding is the primary reason we have so many pensions turning retired government employees into pension millionaires.

The exponential growth of the six statewide Illinois government pension funds continues unabated. These six funds include the General Assembly Retirement System (GARS), Judges Retirement System (JRS), State University Retirement System (SURS), State Employees Retirement System (SERS), Teachers Retirement System (TRS), and the Illinois Municipal Retirement Fund(IMRF).

Some of the key statistics regarding how the pension system is funded are as follows:

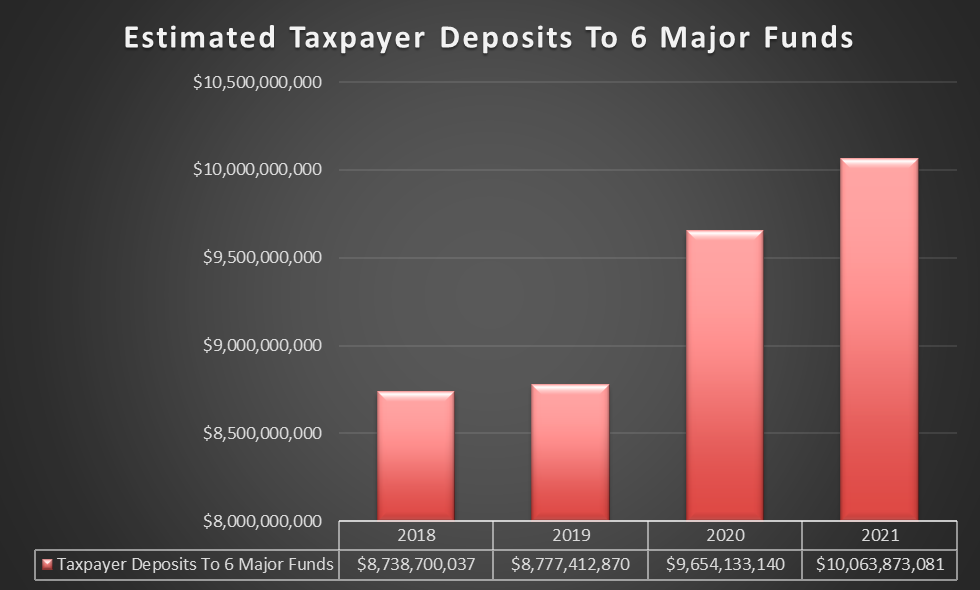

•Taxpayers are estimated to contribute for 2021 ten billion dollars in order to fund the retirement of government employees. This is a one point three billion dollar increase from 2018.

•Taxpayer contributions are still steadily ramping upwards year over year, despite the recession.

•For the year 2021, estimated employee contributions to their own pensions are down an estimated $35 million from last year.

•The reported net position of the six state wide funds worsened another $4 billion from last year.

Some of the key statistics regarding how the pension system is funded are as follows:

•Taxpayers are estimated to contribute for 2021 ten billion dollars in order to fund the retirement of government employees. This is a one point three billion dollar increase from 2018.

•Taxpayer contributions are still steadily ramping upwards year over year, despite the recession.

•For the year 2021, estimated employee contributions to their own pensions are down an estimated $35 million from last year.

•The reported net position of the six state wide funds worsened another $4 billion from last year.

It is important to remember that taxpayer payments happen regardless of the state budget condition. While taxpayers are losing their jobs and the state coffers run dry during the pandemic, retired state employees retain an iron grip on taxpayers’ wallets. Taxpayers are also the primary source of funding for these massive pensions.

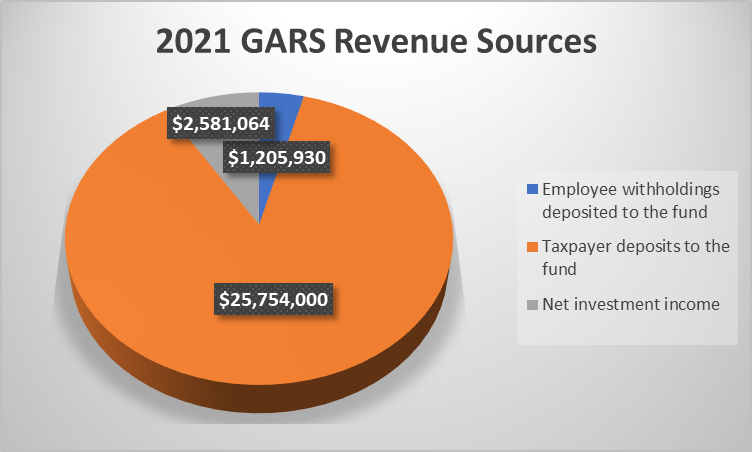

There is a wide spread narrative that the pensions are largely funded by both employee deposits and robust returns on investment. The facts, don’t bear that out. While the state of each individual pension fund is different, some like the General Assembly Retirement System refute any notion of self-reliance. For every dollar from either politicians or investments, taxpayers added an estimated $6.80 to the General Assembly Retirement System. Taxpayers pay more, and will continue to pay more into this broken system for the foreseeable future.

With the current funding requirements, all but the IMRF funding falls extremely short of necessary levels to pay every promised government employee pension.

TRS 40.5%

JRS 37.9%

GARS 16.5%

SERS 38.7%

SURS 42.2%

IMRF 90%

Although the IMRF funding level is in the proper range for a viable schedule of amortization, it doesn’t illustrate the extreme burden that this places on property owners. Illinois statute requires that IMRF pension deposits be paid by taxpayers before any other liabilities.. Under these extremes, taxpayers are being forced out of their homes because they can’t afford IMRF driven property taxes and housing expenses. Additionally, this requirement forces local governments to sacrifice services needed today in order to pay for services rendered in years past.

TEF has and does advocate for pension reforms, included but not limited to: Place all new government hires into a defined contribution account as opposed to the current defined benefit system. Immediately discontinue the automatic cost of living adjustment and make promises to only increase cost of living in alignment with current financial conditions. Remove all of the loopholes that allow salary spiking during the last years of employment on which pension calculations are made.

Click Here to view Top 200 TRS Pensions

Click Here to view Top 200 JRS Pensions

Click Here to view Top 200 GARS Pensions

Click Here to view Top 200 SERS Pensions

Click Here to view Top 200 SURS Pensions

Click Here to view Top 200 IMRF

Click Here To View All $100,000+ Pensions